Vikipedi.org Trusted Information and Education News Media

Vikipedi.org Trusted Information and Education News Media

The latest information about Joint Tenancy With Right Of Survivorship Step-Up In Basis that you need can be found in this article, all of which we have summarized well.

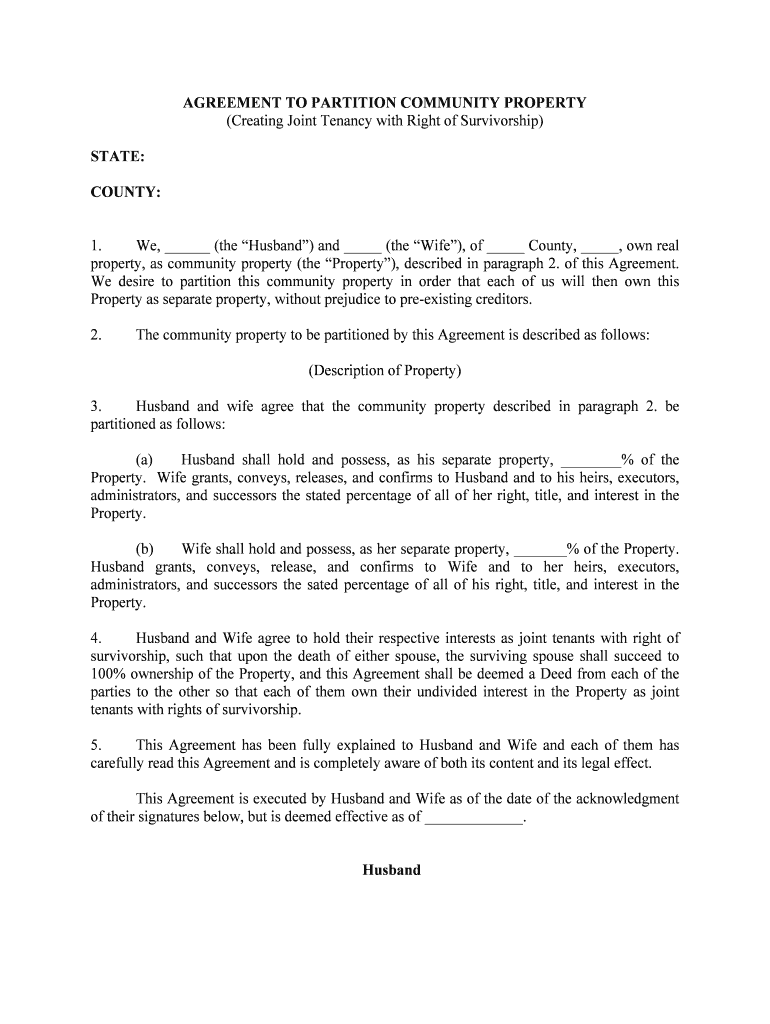

Joint Tenancy with Right of Survivorship and Step-Up in Basis

Life is full of unexpected turns and pivots, and it’s our moments of adversity that truly test our resilience. A dear friend of mine, Emily, faced a tumultuous journey when her beloved husband, John, passed unexpectedly. Amidst the grief and sorrow, Emily was confronted with the complexities of managing their jointly owned assets. It was through this experience that I realized the importance of understanding the legal intricacies surrounding joint tenancy, particularly in situations involving the “right of survivorship” and “step-up in basis.”

Joint tenancy is a form of ownership where two or more individuals hold title to property jointly. The defining characteristic of joint tenancy is the “right of survivorship,” which dictates that upon the death of one owner, their interest in the property automatically transfers to the surviving owner(s). This differs from tenancy in common, where the deceased owner’s share passes according to their will or intestacy laws.

Step-Up in Basis: A Tax-Saving Opportunity

When property is held in joint tenancy with right of survivorship, it also qualifies for a “step-up in basis” upon the death of one joint tenant. This means that the surviving joint tenant(s) receive a new, adjusted cost basis for the property, which is equal to its fair market value as of the date of the deceased joint tenant’s death. This adjustment can result in significant tax savings when the property is eventually sold.

Understanding the Mechanics of Step-Up

To illustrate the step-up in basis concept, let’s consider the following scenario: Emily and John purchased a house together for $500,000. When John passed away, the house was worth $750,000. Under the step-up in basis rule, Emily’s cost basis for the house becomes $750,000, even though she only paid half of the original purchase price. As a result, if she decides to sell the house for $800,000, she will only pay capital gains tax on the difference between the sales price and her new cost basis of $750,000, instead of the original $500,000.

The step-up in basis not only reduces Emily’s potential capital gains tax liability but also increases her depreciation deductions if she intends to rent out the property. Additionally, the stepped-up basis can be passed on to subsequent joint tenants if Emily adds another individual to the deed in the future.

Joint Tenancy Considerations and Cautions

While joint tenancy with right of survivorship offers potential tax benefits, it’s important to consider its implications carefully. Joint ownership means that all joint tenants have equal rights and responsibilities regarding the property, regardless of their financial contributions. This can lead to disputes or complications if the joint tenants have different financial goals or objectives.

Another potential drawback is that joint tenancy limits the deceased joint tenant’s ability to control the disposition of their interest in the property. If a joint tenant wants to ensure that their share passes to a specific beneficiary other than the surviving joint tenant(s), they must create a will or trust to do so.

Tips for Using Joint Tenancy and Step-Up Effectively

If you’re considering joint tenancy with right of survivorship, keep these tips in mind:

- Choose your joint tenants carefully. Choose individuals with whom you have a close and trusting relationship, as joint ownership carries significant legal responsibilities.

- Consider your estate planning goals. Joint tenancy may not be the best option if you have specific intentions for the disposition of your assets upon your death.

- Discuss potential tax implications with a qualified financial advisor. The step-up in basis can provide tax savings, but it’s important to weigh this against other tax considerations.

By carefully planning and understanding the legal and tax implications of joint tenancy with right of survivorship, you can harness its potential benefits while mitigating potential risks. Remember, it’s always advisable to seek professional advice from an attorney and financial advisor to guide you through these complex matters.

FAQs on Joint Tenancy with Right of Survivorship and Step-Up in Basis

- What is the difference between joint tenancy and tenancy in common? Joint tenancy has the right of survivorship, meaning the deceased owner’s interest passes to the surviving owner(s), while tenancy in common allows the deceased owner to pass their share to a chosen beneficiary.

- How does the step-up in basis affect capital gains tax? The step-up in basis reduces the potential capital gains tax liability because the surviving joint tenant receives a new cost basis equal to the property’s fair market value at the time of the deceased joint tenant’s death.

- What are the potential drawbacks of joint tenancy? Joint tenancy limits the deceased joint tenant’s ability to control the disposition of their interest in the property and can lead to disputes if the joint tenants have different financial goals.

- Can I add or remove a joint tenant later on? Yes, adding or removing a joint tenant is possible, but it requires the consent of all current joint tenants and may have tax implications.

- How can a joint tenant protect their share of the property if they are concerned about the other joint tenant? A joint tenant can create a will or trust to ensure that their share of the property passes to a specific beneficiary upon their death, overriding the automatic transfer to the surviving joint tenant(s).

Conclusion

Understanding the intricacies of joint tenancy with right of survivorship and step-up in basis is crucial for individuals looking to optimize their estate planning and tax strategies. By carefully considering the legal and financial implications, you can effectively harness the benefits of joint ownership while mitigating potential risks. Remember, planning ahead and seeking professional advice can empower you to make informed decisions that protect your assets and align with your long-term financial goals. If you have any further questions or require personalized guidance, don’t hesitate to consult with an experienced attorney or financial advisor.

Would you like to know more about joint tenancy with right of survivorship and step-up in basis?

Image: www.signnow.com

Joint Tenancy With Right Of Survivorship Step-Up In Basis has been read by you on our site. We express our gratitude for your visit. We hope you benefit from Joint Tenancy With Right Of Survivorship Step-Up In Basis.

YToxOntzOjExOiJ0aWVfb3B0aW9ucyI7YTo5NDp7czoxMjoidGhlbWVfbGF5b3V0IjtzOjU6ImJveGVkIjtzOjc6ImZhdmljb24iO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6ODoiZ3JhdmF0YXIiO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6MTI6ImFwcGxlX2lwaG9uZSI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxOToiYXBwbGVfaXBob25lX3JldGluYSI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxMDoiYXBwbGVfaVBhZCI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxNzoiYXBwbGVfaVBhZF9yZXRpbmEiO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6MTE6InRpbWVfZm9ybWF0IjtzOjY6Im1vZGVybiI7czoxMjoibGlnaHRib3hfYWxsIjtzOjQ6InRydWUiO3M6MTY6ImxpZ2h0Ym94X2dhbGxlcnkiO3M6NDoidHJ1ZSI7czoxMzoibGlnaHRib3hfc2tpbiI7czo0OiJkYXJrIjtzOjE1OiJsaWdodGJveF90aHVtYnMiO3M6ODoidmVydGljYWwiO3M6MTE6ImJyZWFkY3J1bWJzIjtzOjQ6InRydWUiO3M6MjE6ImJyZWFkY3J1bWJzX2RlbGltaXRlciI7czoxOiIvIjtzOjEyOiJsb2dvX3NldHRpbmciO3M6NDoibG9nbyI7czo0OiJsb2dvIjtzOjY1OiJodHRwczovL3d3dy5od2F0cnIuY29tL3dwLWNvbnRlbnQvdXBsb2Fkcy8yMDIxLzA5L2h3YXRyci1sb2dvLnBuZyI7czoxMToibG9nb19yZXRpbmEiO3M6NjU6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvaHdhdHJyLWxvZ28ucG5nIjtzOjExOiJsb2dvX21hcmdpbiI7czoyOiIxNSI7czoxODoibG9nb19tYXJnaW5fYm90dG9tIjtzOjI6IjE1IjtzOjg6InRvcF9tZW51IjtzOjQ6InRydWUiO3M6MTY6InRvZGF5ZGF0ZV9mb3JtYXQiO3M6OToibCAsIEYgaiBZIjtzOjEwOiJ0b3Bfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTE6ImxpdmVfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTA6InRvcF9zb2NpYWwiO3M6NDoidHJ1ZSI7czo4OiJtYWluX25hdiI7czo0OiJ0cnVlIjtzOjE0OiJyYW5kb21fYXJ0aWNsZSI7czo0OiJ0cnVlIjtzOjk6InN0aWNrX25hdiI7czo0OiJ0cnVlIjtzOjE4OiJtb2JpbGVfbWVudV9hY3RpdmUiO3M6NDoidHJ1ZSI7czoxODoibW9iaWxlX21lbnVfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTg6Im1vYmlsZV9tZW51X3NvY2lhbCI7czo0OiJ0cnVlIjtzOjIyOiJtb2JpbGVfbWVudV9oaWRlX2ljb25zIjtzOjQ6InRydWUiO3M6MTM6ImJyZWFraW5nX25ld3MiO3M6NDoidHJ1ZSI7czoxNToiYnJlYWtpbmdfZWZmZWN0IjtzOjQ6ImZhZGUiO3M6MTQ6ImJyZWFraW5nX3NwZWVkIjtzOjM6Ijc1MCI7czoxMzoiYnJlYWtpbmdfdGltZSI7czo0OiIzNTAwIjtzOjEzOiJicmVha2luZ190eXBlIjtzOjg6ImNhdGVnb3J5IjtzOjE1OiJicmVha2luZ19udW1iZXIiO3M6MjoiMTAiO3M6ODoicnNzX2ljb24iO3M6NDoidHJ1ZSI7czo4OiJwb3N0X25hdiI7czo0OiJ0cnVlIjtzOjEzOiJwb3N0X29nX2NhcmRzIjtzOjQ6InRydWUiO3M6MTE6InNjaGVtYV90eXBlIjtzOjc6IkFydGljbGUiO3M6OToicG9zdF9tZXRhIjtzOjQ6InRydWUiO3M6MTE6InBvc3RfYXV0aG9yIjtzOjQ6InRydWUiO3M6OToicG9zdF9kYXRlIjtzOjQ6InRydWUiO3M6OToicG9zdF9jYXRzIjtzOjQ6InRydWUiO3M6OToicG9zdF90YWdzIjtzOjQ6InRydWUiO3M6MTA6InBvc3Rfdmlld3MiO3M6NDoidHJ1ZSI7czoxMDoic2hhcmVfcG9zdCI7czo0OiJ0cnVlIjtzOjE5OiJzaGFyZV9idXR0b25zX3BhZ2VzIjtzOjQ6InRydWUiO3M6MTU6InNoYXJlX3Bvc3RfdHlwZSI7czo0OiJmbGF0IjtzOjE1OiJzaGFyZV9zaG9ydGxpbmsiO3M6NDoidHJ1ZSI7czoxMToic2hhcmVfdHdlZXQiO3M6NDoidHJ1ZSI7czoxNDoic2hhcmVfZmFjZWJvb2siO3M6NDoidHJ1ZSI7czoxMzoic2hhcmVfbGlua2RpbiI7czo0OiJ0cnVlIjtzOjEzOiJzaGFyZV9zdHVtYmxlIjtzOjQ6InRydWUiO3M6MTU6InNoYXJlX3BpbnRlcmVzdCI7czo0OiJ0cnVlIjtzOjc6InJlbGF0ZWQiO3M6NDoidHJ1ZSI7czoxNjoicmVsYXRlZF9wb3NpdGlvbiI7czo1OiJiZWxvdyI7czoxNDoicmVsYXRlZF9udW1iZXIiO3M6MToiMyI7czoxOToicmVsYXRlZF9udW1iZXJfZnVsbCI7czoxOiI0IjtzOjEzOiJyZWxhdGVkX3F1ZXJ5IjtzOjg6ImNhdGVnb3J5IjtzOjEwOiJjaGVja19hbHNvIjtzOjQ6InRydWUiO3M6MTk6ImNoZWNrX2Fsc29fcG9zaXRpb24iO3M6NToicmlnaHQiO3M6MTc6ImNoZWNrX2Fsc29fbnVtYmVyIjtzOjE6IjEiO3M6MTY6ImNoZWNrX2Fsc29fcXVlcnkiO3M6ODoiY2F0ZWdvcnkiO3M6MTA6ImZvb3Rlcl90b3AiO3M6NDoidHJ1ZSI7czoxMzoiZm9vdGVyX3NvY2lhbCI7czo0OiJ0cnVlIjtzOjIxOiJmb290ZXJfd2lkZ2V0c19lbmFibGUiO3M6NDoidHJ1ZSI7czoxNDoiZm9vdGVyX3dpZGdldHMiO3M6OToiZm9vdGVyLTNjIjtzOjEwOiJmb290ZXJfb25lIjtzOjQwOiLCqSBDb3B5cmlnaHQgJXllYXIlLCBBbGwgUmlnaHRzIFJlc2VydmVkIjtzOjEwOiJmb290ZXJfdHdvIjtzOjY6IiVzaXRlJSI7czoxMToic2lkZWJhcl9wb3MiO3M6NToicmlnaHQiO3M6MTQ6InN0aWNreV9zaWRlYmFyIjtzOjQ6InRydWUiO3M6MTA6ImV4Y19sZW5ndGgiO3M6MjoiNTAiO3M6MTQ6ImFyY19tZXRhX3Njb3JlIjtzOjQ6InRydWUiO3M6MTM6ImFyY19tZXRhX2RhdGUiO3M6NDoidHJ1ZSI7czoxMzoiYXJjX21ldGFfY2F0cyI7czo0OiJ0cnVlIjtzOjE3OiJhcmNfbWV0YV9jb21tZW50cyI7czo0OiJ0cnVlIjtzOjEyOiJibG9nX2Rpc3BsYXkiO3M6NzoiZXhjZXJwdCI7czoxMzoiY2F0ZWdvcnlfZGVzYyI7czo0OiJ0cnVlIjtzOjEyOiJjYXRlZ29yeV9yc3MiO3M6NDoidHJ1ZSI7czoxNToiY2F0ZWdvcnlfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6NzoidGFnX3JzcyI7czo0OiJ0cnVlIjtzOjEwOiJ0YWdfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6MTA6ImF1dGhvcl9iaW8iO3M6NDoidHJ1ZSI7czoxMDoiYXV0aG9yX3JzcyI7czo0OiJ0cnVlIjtzOjEzOiJhdXRob3JfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6MTM6InNlYXJjaF9sYXlvdXQiO3M6NzoiZXhjZXJwdCI7czoxMDoidGhlbWVfc2tpbiI7czo3OiIjZWYzNjM2IjtzOjIwOiJob21lcGFnZV9jYXRzX2NvbG9ycyI7czo0OiJ0cnVlIjtzOjk6ImxhenlfbG9hZCI7czo0OiJ0cnVlIjtzOjE1OiJiYWNrZ3JvdW5kX3R5cGUiO3M6NzoicGF0dGVybiI7czoxODoidHlwb2dyYXBoeV9nZW5lcmFsIjthOjE6e3M6NDoiZm9udCI7czoyMjoiRHJvaWQgU2FuczpyZWd1bGFyfDcwMCI7fXM6MTI6Im5vdGlmeV90aGVtZSI7czo0OiJ0cnVlIjt9fQ==

YToxOntzOjExOiJ0aWVfb3B0aW9ucyI7YTo5NDp7czoxMjoidGhlbWVfbGF5b3V0IjtzOjU6ImJveGVkIjtzOjc6ImZhdmljb24iO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6ODoiZ3JhdmF0YXIiO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6MTI6ImFwcGxlX2lwaG9uZSI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxOToiYXBwbGVfaXBob25lX3JldGluYSI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxMDoiYXBwbGVfaVBhZCI7czo3MzoiaHR0cHM6Ly93d3cuaHdhdHJyLmNvbS93cC1jb250ZW50L3VwbG9hZHMvMjAyMS8wOS9jcm9wcGVkLWh3YXRyci1pY29uLnBuZyI7czoxNzoiYXBwbGVfaVBhZF9yZXRpbmEiO3M6NzM6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvY3JvcHBlZC1od2F0cnItaWNvbi5wbmciO3M6MTE6InRpbWVfZm9ybWF0IjtzOjY6Im1vZGVybiI7czoxMjoibGlnaHRib3hfYWxsIjtzOjQ6InRydWUiO3M6MTY6ImxpZ2h0Ym94X2dhbGxlcnkiO3M6NDoidHJ1ZSI7czoxMzoibGlnaHRib3hfc2tpbiI7czo0OiJkYXJrIjtzOjE1OiJsaWdodGJveF90aHVtYnMiO3M6ODoidmVydGljYWwiO3M6MTE6ImJyZWFkY3J1bWJzIjtzOjQ6InRydWUiO3M6MjE6ImJyZWFkY3J1bWJzX2RlbGltaXRlciI7czoxOiIvIjtzOjEyOiJsb2dvX3NldHRpbmciO3M6NDoibG9nbyI7czo0OiJsb2dvIjtzOjY1OiJodHRwczovL3d3dy5od2F0cnIuY29tL3dwLWNvbnRlbnQvdXBsb2Fkcy8yMDIxLzA5L2h3YXRyci1sb2dvLnBuZyI7czoxMToibG9nb19yZXRpbmEiO3M6NjU6Imh0dHBzOi8vd3d3Lmh3YXRyci5jb20vd3AtY29udGVudC91cGxvYWRzLzIwMjEvMDkvaHdhdHJyLWxvZ28ucG5nIjtzOjExOiJsb2dvX21hcmdpbiI7czoyOiIxNSI7czoxODoibG9nb19tYXJnaW5fYm90dG9tIjtzOjI6IjE1IjtzOjg6InRvcF9tZW51IjtzOjQ6InRydWUiO3M6MTY6InRvZGF5ZGF0ZV9mb3JtYXQiO3M6OToibCAsIEYgaiBZIjtzOjEwOiJ0b3Bfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTE6ImxpdmVfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTA6InRvcF9zb2NpYWwiO3M6NDoidHJ1ZSI7czo4OiJtYWluX25hdiI7czo0OiJ0cnVlIjtzOjE0OiJyYW5kb21fYXJ0aWNsZSI7czo0OiJ0cnVlIjtzOjk6InN0aWNrX25hdiI7czo0OiJ0cnVlIjtzOjE4OiJtb2JpbGVfbWVudV9hY3RpdmUiO3M6NDoidHJ1ZSI7czoxODoibW9iaWxlX21lbnVfc2VhcmNoIjtzOjQ6InRydWUiO3M6MTg6Im1vYmlsZV9tZW51X3NvY2lhbCI7czo0OiJ0cnVlIjtzOjIyOiJtb2JpbGVfbWVudV9oaWRlX2ljb25zIjtzOjQ6InRydWUiO3M6MTM6ImJyZWFraW5nX25ld3MiO3M6NDoidHJ1ZSI7czoxNToiYnJlYWtpbmdfZWZmZWN0IjtzOjQ6ImZhZGUiO3M6MTQ6ImJyZWFraW5nX3NwZWVkIjtzOjM6Ijc1MCI7czoxMzoiYnJlYWtpbmdfdGltZSI7czo0OiIzNTAwIjtzOjEzOiJicmVha2luZ190eXBlIjtzOjg6ImNhdGVnb3J5IjtzOjE1OiJicmVha2luZ19udW1iZXIiO3M6MjoiMTAiO3M6ODoicnNzX2ljb24iO3M6NDoidHJ1ZSI7czo4OiJwb3N0X25hdiI7czo0OiJ0cnVlIjtzOjEzOiJwb3N0X29nX2NhcmRzIjtzOjQ6InRydWUiO3M6MTE6InNjaGVtYV90eXBlIjtzOjc6IkFydGljbGUiO3M6OToicG9zdF9tZXRhIjtzOjQ6InRydWUiO3M6MTE6InBvc3RfYXV0aG9yIjtzOjQ6InRydWUiO3M6OToicG9zdF9kYXRlIjtzOjQ6InRydWUiO3M6OToicG9zdF9jYXRzIjtzOjQ6InRydWUiO3M6OToicG9zdF90YWdzIjtzOjQ6InRydWUiO3M6MTA6InBvc3Rfdmlld3MiO3M6NDoidHJ1ZSI7czoxMDoic2hhcmVfcG9zdCI7czo0OiJ0cnVlIjtzOjE5OiJzaGFyZV9idXR0b25zX3BhZ2VzIjtzOjQ6InRydWUiO3M6MTU6InNoYXJlX3Bvc3RfdHlwZSI7czo0OiJmbGF0IjtzOjE1OiJzaGFyZV9zaG9ydGxpbmsiO3M6NDoidHJ1ZSI7czoxMToic2hhcmVfdHdlZXQiO3M6NDoidHJ1ZSI7czoxNDoic2hhcmVfZmFjZWJvb2siO3M6NDoidHJ1ZSI7czoxMzoic2hhcmVfbGlua2RpbiI7czo0OiJ0cnVlIjtzOjEzOiJzaGFyZV9zdHVtYmxlIjtzOjQ6InRydWUiO3M6MTU6InNoYXJlX3BpbnRlcmVzdCI7czo0OiJ0cnVlIjtzOjc6InJlbGF0ZWQiO3M6NDoidHJ1ZSI7czoxNjoicmVsYXRlZF9wb3NpdGlvbiI7czo1OiJiZWxvdyI7czoxNDoicmVsYXRlZF9udW1iZXIiO3M6MToiMyI7czoxOToicmVsYXRlZF9udW1iZXJfZnVsbCI7czoxOiI0IjtzOjEzOiJyZWxhdGVkX3F1ZXJ5IjtzOjg6ImNhdGVnb3J5IjtzOjEwOiJjaGVja19hbHNvIjtzOjQ6InRydWUiO3M6MTk6ImNoZWNrX2Fsc29fcG9zaXRpb24iO3M6NToicmlnaHQiO3M6MTc6ImNoZWNrX2Fsc29fbnVtYmVyIjtzOjE6IjEiO3M6MTY6ImNoZWNrX2Fsc29fcXVlcnkiO3M6ODoiY2F0ZWdvcnkiO3M6MTA6ImZvb3Rlcl90b3AiO3M6NDoidHJ1ZSI7czoxMzoiZm9vdGVyX3NvY2lhbCI7czo0OiJ0cnVlIjtzOjIxOiJmb290ZXJfd2lkZ2V0c19lbmFibGUiO3M6NDoidHJ1ZSI7czoxNDoiZm9vdGVyX3dpZGdldHMiO3M6OToiZm9vdGVyLTNjIjtzOjEwOiJmb290ZXJfb25lIjtzOjQwOiLCqSBDb3B5cmlnaHQgJXllYXIlLCBBbGwgUmlnaHRzIFJlc2VydmVkIjtzOjEwOiJmb290ZXJfdHdvIjtzOjY6IiVzaXRlJSI7czoxMToic2lkZWJhcl9wb3MiO3M6NToicmlnaHQiO3M6MTQ6InN0aWNreV9zaWRlYmFyIjtzOjQ6InRydWUiO3M6MTA6ImV4Y19sZW5ndGgiO3M6MjoiNTAiO3M6MTQ6ImFyY19tZXRhX3Njb3JlIjtzOjQ6InRydWUiO3M6MTM6ImFyY19tZXRhX2RhdGUiO3M6NDoidHJ1ZSI7czoxMzoiYXJjX21ldGFfY2F0cyI7czo0OiJ0cnVlIjtzOjE3OiJhcmNfbWV0YV9jb21tZW50cyI7czo0OiJ0cnVlIjtzOjEyOiJibG9nX2Rpc3BsYXkiO3M6NzoiZXhjZXJwdCI7czoxMzoiY2F0ZWdvcnlfZGVzYyI7czo0OiJ0cnVlIjtzOjEyOiJjYXRlZ29yeV9yc3MiO3M6NDoidHJ1ZSI7czoxNToiY2F0ZWdvcnlfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6NzoidGFnX3JzcyI7czo0OiJ0cnVlIjtzOjEwOiJ0YWdfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6MTA6ImF1dGhvcl9iaW8iO3M6NDoidHJ1ZSI7czoxMDoiYXV0aG9yX3JzcyI7czo0OiJ0cnVlIjtzOjEzOiJhdXRob3JfbGF5b3V0IjtzOjc6ImV4Y2VycHQiO3M6MTM6InNlYXJjaF9sYXlvdXQiO3M6NzoiZXhjZXJwdCI7czoxMDoidGhlbWVfc2tpbiI7czo3OiIjZWYzNjM2IjtzOjIwOiJob21lcGFnZV9jYXRzX2NvbG9ycyI7czo0OiJ0cnVlIjtzOjk6ImxhenlfbG9hZCI7czo0OiJ0cnVlIjtzOjE1OiJiYWNrZ3JvdW5kX3R5cGUiO3M6NzoicGF0dGVybiI7czoxODoidHlwb2dyYXBoeV9nZW5lcmFsIjthOjE6e3M6NDoiZm9udCI7czoyMjoiRHJvaWQgU2FuczpyZWd1bGFyfDcwMCI7fXM6MTI6Im5vdGlmeV90aGVtZSI7czo0OiJ0cnVlIjt9fQ==